Detailed presentation

This section is structured as follows:

- Definition

- Why and when is a cost-effectiveness analysis undertaken

- How is a cost-effectiveness analysis undertaken

- Examples

- Bibliography

| DEFINITION |

|

What is a cost-effectiveness analysis? A comparative methodology for economic evaluations Purpose Cost-effectiveness analysis identifies the economically most efficient way to fulfil an objective. Focused on the targeted major result of the activity(for example, the number of jobs created), the tool associates the effectiveness of a programme with its cost. Definition The costs are the expenses planned for the implementation of a programme. The effectiveness of an evaluation lies in the relationship results and objectives. The objective of cost-effectiveness analysis is to estimate the cost of the result's implementation. If we take the above example, the analysis estimates the cost of each job generated by a specific measure. A comparative tool The tool compares policies, programmes, or projects (for example, the costs of different programmes with similar impacts - which requires the identification of situations sufficiently similar to allow relevant comparisons). Conversely, in activities with similar costs, results and outcomes are compared. The tool presents alternatives, in order to identify the most appropriate one to achieve an result at least cost. Fields of application Decision-making assistance Cost-effectiveness analysis is especially used in the context of the assistance to decision-making in public policies and programmes, and in public and private investments. In fields such as health, education, environment, employment, and road safety, cost-effectiveness analysis is frequently used to compare complex policies, although the tool is appropriate for other fields. Analysis of activities The tool is generally more appropriate for the analysis of clearly defined activities (in which costs and impacts are easily identifiable), than for the collection of information supporting the analysis of activities, whose sources are varied. The tool is not suitable for the analysis of multiple impact activities, whose effects are varied and difficult to rank. |

|

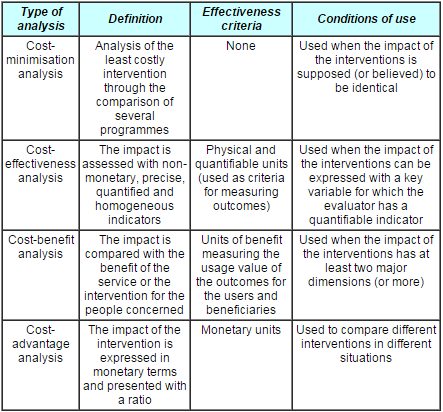

What are the specificities of cost-effectiveness alalysis? Its place among economic evaluation tools Cost-effectiveness analysis belongs to the economic analytical tools which assess per se or comparatively the effectiveness or efficiency of a policy or a programme. Various economic analysis tools available for comparing intervention programmes

Image

In addition to these tools, some authors include cost-feasibility analysis which assesses the feasibility of a policy with the estimation of the costs it generates. |

|

Effectiveness measured with a single outcome In order to measure the effectiveness of a policy or a programme, the tool focuses on the main expected impact of the intervention. The analysis does not consider other impacts of the policy or programme, whether they are targeted impacts or not. Determination of a relevant outcome

Image

|

|

A measure based on a physical basis, not a monetary one The other specificity of cost-effectiveness analysis is to measure the effectiveness with indicators highlighting results and outcomes. Contrary to cost-advantage analysis, cost-effectiveness analysis does not evaluate the monetary value of the outcomes. Thus, it is an economic (and not a financial) analysis methodology.

|

|

Which questions can a cost-effectiveness analysis answer? Cost-effectiveness analysis may contribute to answers to the following questions:

. |

| WHY AND WHEN IS A COST-EFFECTIVENESS ANALYSIS UNDERTAKEN? |

|

. What are the possible uses of cost-effectiveness analysis in evaluations? In the context of a co-operation assistance policy evaluation, cost-effectiveness analysis can be used as an evaluation tool dedicated to projects, programmes or sectors. It is an economic tool which analyses operational objectives at various levels. Conversely, it is not adapted to country strategy analyses, except when the strategy focuses on a single objective, whose implementation targets a clearly identifiable result. Possible uses of cost-effectiveness analysis depending on the type of evaluation

Image

At the start of the evaluation It can be useful to choose the programmes or projects which will be the subject of a cost-effectiveness analysis at the start of the evaluation. Indeed, selecting the programmes with prioritised co-operation objectives, and impacts which are measured in homogeneous units, avoids making distracting analyses of efficiency and impact during the evaluation. To assess the choices in the allocation of resources The process of drafting and negotiation of national co-operation strategies require the distribution of limited resources between programmes. Various factors influence this distribution, such as questions of sensitivity, acceptability, equity and effectiveness. To determine strategy planning priorities Cost-effectiveness analysis is a valuable tool for defining the strategy planning priorities. It enables decision-makers to determine priorities in relation to the costs and consequences (in terms of simple quantitative results) of the various possible initiatives needed for the achievement of a pre-established objective. To conduct a complex debate Determining the priorities among the results, quantifying and homogenising indicators of outcome constitute the crucial stages of a country evaluation. |

|

Within which type of evaluation can it be conducted? Undertaking cost-effectiveness analysis in the context of an ex ante, intermediary or ex post evaluation generates various methodological challenges and a complex information collection operation during the implementation stage. In ex ante evaluations Cost-effectiveness analysis is primarily used to support decision-making. It determines whether a decision to intervene is economically well grounded, or which intervention among others is the most efficient. Thus, this type of analysis is particularly designed for ex ante evaluations, to judge the economic relevance of a measure to be taken. In ex post evaluations In ex post evaluations, the analysis can contribute to the measurement of the economic efficiency of an intervention already carried out. For the same intervention, ex post and ex ante analyses can yield different outcomes, for example, because unexpected costs have become necessary for the achievement of the objectives, or because the outcomes are different from the expected results. In intermediate evaluations The analysis can be very useful for intermediate evaluations as a means to update the ex ante outcomes and choose which options should be selected for the continuation of the intervention. |

|

What are its advantages and limitations? Advantages An ex ante evaluation tool Cost-effectiveness analysis is a simple and effective tool which compares different measures or programmes with identical objectives. It is a valuable tool for ex ante evaluations, because it facilitates the selection of various interventions on the basis of their cost. An educational and communicational tool Cost-effectiveness analysis summarises the outcomes using a single quantifiable indicator. It expresses in a simple and factual way a single priority objective in an intervention, which has informative and communications value. Visibility of the intervention's effectiveness Cost-effectiveness analysis presents the costs of the results of the intervention to beneficiaries and decision-makers, who often appreciate such a simple and factual illustration of the intervention's objectives. Limitations Cost-effectiveness analysis focuses on the main direct outcome of the intervention. Focusing on the main impact means neglecting indirect impacts. Indeed, the analysis compares costs to immediate outcomes, and neglects long-term impacts.

Cost-effectiveness analysis can determine whether or not an intervention is economically efficient and, more specifically, if it is comparatively more efficient. Conversely, the analysis does not determine whether the intervention's implementation is relevant or appropriate. Difficulties of the ex post evaluation In the context of an ex post evaluation, cost-effectiveness analysis requires reliable data on the real costs of the intervention and on its outcomes. |

|

With which tools can it be combined? With a cost-advantage analysis The outcomes analysis is not limited to the study of direct positive outcomes. The evaluator should also quantify negative impacts, as well as indirect and multiplier impacts, which are difficult to measure precisely. Yet, an estimation may still be valuable, to give a more accurate picture of the effective outcomes. Cost-effectiveness analysis can produce these estimations. With a multicriteria analysis To assess programmes or national (or regional) co-operation strategies characterised by numerous and complex impacts (direct and indirect, positive and negative), the evaluator should use weighting systems on the results. These compound methodologies (such as multicriteria analysis) can be combined with cost-effectiveness analysis or used on its own. . |

| HOW IS A COST-EFFECTIVENESS ANALYSIS UNDERTAKEN? |

|

. STAGE 1: Define the conditions for its use Conditions for the implementation of cost-effectiveness analysis

Image

Check the relevance of the analysis to the objectives of the programme This stage checks whether cost-effectiveness analysis constitutes a relevant analytical tool for the programme under study. Identify the availability and reliability of the data Before undertaking cost-effectiveness analysis, the availability and reliability of the data relating to the costs and the quantitative indicator on the results and outcomes should be checked. The analysis requires reliable data, i.e.:

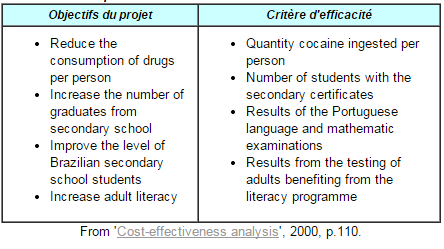

Determine the effectiveness criteria and develop the relevant indicator Selection of the effectiveness criteria Once the feasibility of cost-effectiveness analysis is confirmed, the choice of the effectiveness criteria depends on the main objective of the intervention. Example of the selection of effectiveness criteria

Image

Selection of a relevant criteria The development of criteria depends on several factors. In many countries, the scarce and limited reliability of statistical sources limits the range of choices. Thus, finding means of observation required for the use of an indicator is crucial. |

|

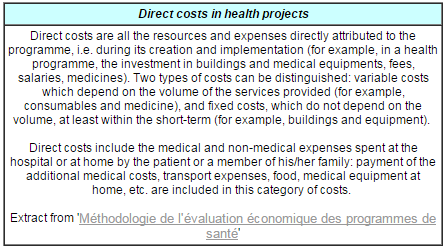

STAGE 2: Evaluate the total cost of the programme Add direct costs In the context of the analysis of the development assistance intervention, the simplest and more commonly used methodology consists of adding all the public resources used in the programme. In this type of calculation, only the direct costs invested in the intervention are considered. These costs are often financial: subventions, financial transfers, decreases in taxes, financing of projects and activities, etc. Direct costs calculation

Image

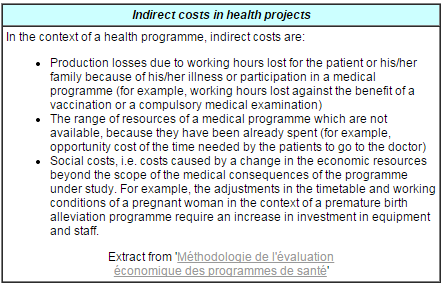

Examine indirect costs Indirect costs, such as the costs of human resources required for the management of programmes, indicate the value of civil servants' work in charge of monitoring the programme or intervention. They should be taken into account whenever they constitute an important part of the intervention's costs. Indirect costs calculation

Image

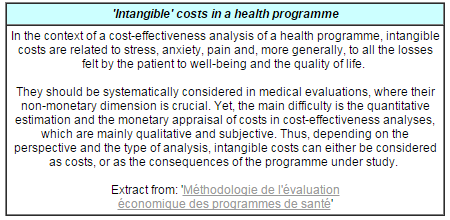

Examine other types of costs Cost calculations can include the loss of earnings and benefits due to the fact that public financing have been attributed to a specific objective (this is called the lost opportunity cost). Calculation of other costs

Image

|

|

STAGE 3: Measure the impact of the programme This is the most difficult stage of the process. Preconditions: nature of the information The study of the programme's impact depends on the nature of the information at the disposal of the evaluator. Ex ante evaluations In ex ante evaluations, the evaluator must forecast the quantitative results of the programme. Depending on the complexity of the intervention, the use of simulation techniques may be required. Ex post evaluations In ex post evaluations, the evaluator can use empirical techniques if the primary data at his/her disposal are sufficiently numerous and reliable. If not, the evaluator needs to estimate the actual quantitative results from secondary data.

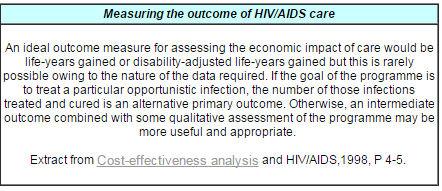

Example Impact measure

Image

|

|

STAGE 4: Establish a cost-to-effectiveness ratio Comparison The analysis requires stable elements to support the comparison between:

Comparison of programmes with identical outcomes When the analysis compares different programmes with identical outcomes, the study is straightforward because the chosen parameter is the cost comparison criteria. Comparison of programmes with identical costs When, for the same objective, the analysis compares different types of interventions with identical costs, the study becomes challenging. Decision-making Decision-making is usually political. The evaluator uses cost-effectiveness analysis as a decision-making assistance tool designed to facilitate the decision. Develop and lead the process of thinking The tool can be used:

Combine cost-effectiveness analysis with multicriteria analysis Cost-effectiveness analysis is not a sufficient tool to conduct a debate between the representatives of various interests and help them define priorities together. It must be supported by a multicriteria analysis. In this context, cost-effectiveness analysis constitutes the first stage of the multicriteria analysis. Example Cost-effectiveness ratio

Image

|

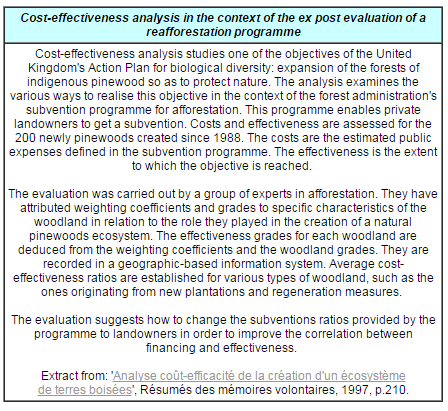

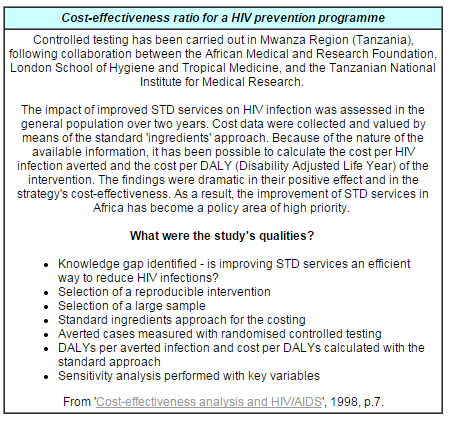

| EXAMPLES |

| Bibliography |

|

|