4.3.1 Social Protection

The expansion of social protection is key for policies aiming at encouraging the transition from the informal to the formal economy. For this reason, major international actors are focusing on this goal, also included among SDGs.

Universal social protection is goal 1.3 of the SDGs: “Implement nationally appropriate social protection systems and measures for all, including floors, and by 2030 achieve substantial coverage of the poor and vulnerable”and there are many other related targets.

|

Box 20 - Other Social Protection related targets goals

|

As early as 2011, the African Union adopted a Social Protection Plan for the Informal Economy and Rural Workers (SPIREWORK), “in recognition of significant contribution of the informal economy to GDP, jobs creation, poverty alleviation, social cohesion and political stability in Africa”. The African Union acknowledges that “social protection (…) has the potential to be the backbone of any strategy towards the modernization or (…) formalisation of the informal economy” (African Union, 2011).

Various coalitions, partnerships and initiatives have emerged to deal with these issues: the Inter-agency Social Protection Assessments (https://ispatools.org/) that defines social protection as a set of policies and programs aimed at preventing or protecting all people against poverty, vulnerability and social exclusion, and designed a Core Diagnostic Instrument (CODI), in partnership with the major international institutions and bilateral donors; the EU Social Protection Systems Programme (http://www.oecd.org/dev/inclusivesocietiesanddevelopment/eu-social-protection-systems-programme.htm), in partnership with OECD and Finland; and the platform Socialprotection.org (http://socialprotection.org/), which aims at promoting knowledge sharing and capacity building on social protection policies.

The World Bank and the ILO also decided to gather their efforts in a Universal Social Protection Initiative towards the achievement of SDGs goal 1.3 (World Bank and ILO, 2015). “Achieving universality would facilitate the delivery of the World Bank’s corporate goals of reducing poverty and increasing shared prosperity and the ILO’s mandate of promoting decent work and social protection for all” (and could we add now, the transition from the informal to the formal economy).

In the following sections, after a brief reminder of the variety of systems of social protection and the variety of risks covered, some national policies will be presented, then the role and impact of projects will be emphasised for the extension of social protection among the vulnerable populations dependent on the informal economy. Lastly a few significant social safety nets and public works programs will be analysed.

1. Variety of schemes: social security, social assistance and safety nets[1]

Social protection is a very broad notion and a generic term that comprises several dimensions and can be understood differently according to countries and regions. It is comprised of two main components: social security and social assistance (also called social safety nets).

- ‘Social security’ which is based on workers’ contributions that employers and their employees as well as the self-employed pay. It provides benefits to workers and all their entitled family members who are inactive and therefore dependent.

- ‘Social assistance’ - safety nets - that governments provide. These are financed through taxes and generally, though not always, target poor and vulnerable populations.

Reflexions on social protection remain marked by the type of funds that are mobilised to cover the risks: contributions based on salaries or more generally on income from work (Bismarckian systems), or contributions paid through taxes (Beveridgian systems). With the increasing concern for competitiveness, the tendency has been more and more oriented towards mixed systems in order to alleviate the contributions on salaries and to balance the deficits of the Bismarckian systems with increased recourse to taxation.

At the roots of social protection there are the social security systems that have been put in place by the States for civil servants and workers in the public sector and later on extended to the private formal sector. Depending on countries, social security covers one or several, or all of the following risks:

- Health and sick leave;

- Maternity and maternity leave;

- Old-age pensions;

- Unemployment benefits;

- Insurance against occupational injuries and diseases.

There are as many systems as there are countries: in some countries, the social security covers all risks and the contributions are paid by the employers and the employees; in other countries, it is limited to pensions and the contribution to health coverage is left to the individuals who have the obligation to pay their insurance premium to a public or a private institution.

The legal framework for social protection is characterised by a variety of situations that themselves depend on the level of development and the structure of the economy. Countries with a large agricultural sector and a broad informal economy and consequently with a tight wage employment have necessarily a different approach than countries with a wide social security system based on contributions collected on salaries and labour income.

Since the adoption of the ILO’s Recommendation 202 on social protection floors in 2012, and of the ILO’s Recommendation 204 on transitioning from the informal to the formal economy in 2015, many countries have given more emphasis to their social policies, all the more so as their traditional formal systems of social protection have given signs of unsustainability and disequilibria between expenditures and resources due to the expansion of the informal economy and the ageing of their populations.

Today several types of social security systems can be observed and depending on the countries, several or all of the risks are covered by public agencies or Funds, whereas in other countries the private sector is in charge of the collection of the contributions from the beneficiaries:

- Pure contributory systems covering all risks for all categories of workers (in Tunisia for instance), combined with a redistributive system of social assistance for the vulnerable populations that escape the social security. With the ageing of population and the rise of unemployment and underemployment, such systems are under pressure and have more and more been seen as a “charge” on salaries (rather than an insurance premium paid by the beneficiaries) dis-incentivising employers from hiring, and pushing governments towards revising the degree of coverage and the number of beneficiaries;

- Contributory systems limited to old-age pensions and to the formal sector and the recourse to the private sector for health coverage (Côte d’Ivoire for instance);

- Mixed systems limiting the risks and the categories of workers benefiting of a contributory system and organising the contribution for other risks and for other categories of population through the private sector.

As anyone can easily imagine, such systems have difficulties to become universal because in many countries paid employment represents a small share of the active population: this is particularly the case in countries where agriculture and/or informal self-employment is widespread. Although the contributory systems have been extended to self-employment and to many if not all kinds of occupations, the coverage of social security fails to be universal. This is whysocial assistance programmes (“social safety nets”) have been generalised that consists in providing targeted populations with coverage for some of the risks at the costs of the taxpayer (redistributive systems).

Depending on the type of system, projects can target specific populations and support them in accessing to adapted health coverage through cooperative or mutual insurances.

Moreover, in the absence of state support, vulnerable populations may quasi-exclusively rely on self-help groups that can provide assistance to their members in need. Extended families provide support to cover health expenditures, unemployment, and other benefits and allowances. It has been shown (Charmes, 2003) that in sub-Saharan Africa in the 1980’-1990s for instance, monetary and in-kind transfers between households – including remittances - represented as much as 25% of the average household income, that is a share equivalent to social expenditures or public transfers in European countries.

Social protection systems thus have three dimensions:

- An insurance dimension that relates to the formal sector;

- An assistance dimension that relates to vulnerable populations uncovered by social security;

- A community-based dimension.

Social security is a form of social insurance for paid employees (and also for the self-employed) and their family dependents – spouses, children under a certain age or disabled, old aged parents. Social security covers various risks related to health, family, old age, unemployment, etc.

In its broad sense (vertically), social security aims to guarantee protection against:

§ absence or insufficiency of income from work, due to sickness, invalidity, maternity, accidents at work and occupational diseases, unemployment, old age, decease of a family member,

- Lack of or unaffordable access to health care;

- Insufficiency of family support, especially for children and dependent adults;

- Poverty and social exclusion in general.

Horizontally, social security has been extended to most economic activities and professions, and all statuses in employment: agriculture, fishery, domestic workers, the self-employed, etc. In some countries, however, some of these activities and statuses still remain uncovered.

It is usually admitted that social security is an advantage provided to employees of the formal sector and is not accessible to people working in the informal economy. This is because, in many countries, social contributions are based on salaries with wage-earners paying a part of the contributions and employers paying another part (generally higher). It is a compulsory formal economy insurance mechanism. This is why both employers and employees-beneficiaries have usually interpreted it as a tax or a cost. The levels of contributions have increased together with the cost of social expenditures and the life expectancy and ageing of populations.

The rising cost of social security has become a handicap in companies’ competitiveness. This has led governments to adopt measures to restrict health expenditures and pensions in many countries. It has also led informal economy entrepreneurs not to declare their workers or to declare them at a minimum wage level instead of their “real” salary.

Social assistance generally benefits the poor and vulnerable. It consists in free access to healthcare, conditional (or not) cash transfers, or transfers in kind. Traditionally, Ministries of Social Affairs draw up lists of persons or families in distress. This may include persons with disabilities, elderly or female-headed households, or large households. The transfers are intended to help them meet their consumption needs or support their income-generating activities through transfers of small equipment or livestock. An example of the latter is the National Programme for Needy Families in Tunisia.

Safety nets are diverse: In 2015, the World Bank assessed the state of social safety nets at world level (World Bank, 2015). From price subsidies on basic goods or cash transfers that have sometimes become conditional to infants’ vaccination and children’s schooling (behavioural conditions) or subject to several criteria (such as income levels or demographic or socio-economic characteristics), to the provision of a number of workdays through labour intensive public works, there is a huge variety of safety nets. The most well-known and successful of these conditional cash transfers programmes is the Brazilian “Bolsa Familia” that dramatically lowered the national poverty rate. Such schemes are, however, often criticised for their deficient targeting, especially when non-conditional.

Safety nets, conditional cash transfers, and targeted programs are options for both the states and the projects: There is a relatively strict correspondence between the goals of social protection systems and the objectives of specific projects: In this sense, many projects can be considered as safety nets ensuring the benefit of income generating jobs to the targeted populations, and the related issue to be discussed is then how to make the actions of the projects sustainable in the longer term, that is, beyond the duration of the project.

Self-help community-based saving and lending groups are also widespread in traditional societies in developing countries, especially in sub-Saharan Africa (see for instance Vuarin, 1993 and 2000 for Mali; and Oduro, 2010 for the interplay between formal and informal systems of social protection). They represent an important aspect of microfinance. Through these groups, members are led to save and they can use their right to borrow in order to meet their consumption or investment needs. Members may also use their savings as a micro-insurance mechanism to fall back on when they are affected by health risks. Poor populations dependent on the informal economy may be convinced and led toward saving on a daily or weekly basis – or as often as you can - in order to accumulate some funds that will make them eligible to mutual insurance institutions. AVSI in Côte d’Ivoire (one of the 17 EC-funded projects partnering with RNSF) is in such an approach with associations of handicrafts in several regions of the country.

An increasing trend in micro-finance institutions is to offer micro-insurance - including protection against the impact of crop failures, death of relatives, or chronic health issues. Many EU projects aimed at enhancing livelihoods for poor populations dependent on the informal economy include such actions.

1.1 Social Safety nets

At world level, more than 1.9 billion people are covered by social safety nets (and among them, more than 526 million people are enrolled in the 5 major social safety nets). Yet, globally only one-third of the poor are covered. In average, a developing country runs about 20 different safety nets. Total spending in social safety nets totalled twice the amount needed to provide every person living in extreme poverty with an income of 1.25 US$ a day. However it represents much less than the amount of subsidies on fuel, which are possibly assumed to have crowded out public spending on social safety nets and pro-poor policies.

The World Bank has recently published a comprehensive assessment of social safety nets around the world (World Bank, 2015).

The World Bank distinguishes six types of social safety nets programs (see Chart 1 below): Conditional Cash Transfers (CCT), Unconditional Cash Transfers (UCT: targeted to the elderly, the handicapped, children, etc.), School Feeding Programs, Unconditional in-kind Transfers (such as food), Public Works Programs, and Fee waivers (assisting households for covering the costs of education, health and housing).

The assessment established by the World Bank shows that in 2015 school feeding and unconditional cash transfers were the most widespread programs with 131 and 130 countries respectively (out of 157) followed by public works (94 countries), unconditional in-kind transfers (92), then conditional cash transfers (63) and lastly fee waivers (49). In number of beneficiaries, Bolsa Familia is the most important of the CCTs (45 million representing 24% of the population) and Di-Bao (China) for the UCTs (75 million), whereas India comes first for the public works with MGNREGA (Mahatma Gandhi National Rural Employment Guarantee Act: 58 million beneficiaries).

It is admitted that the typical cash transfers programs in lower income countries do not provide adequate income support covering only 10% of the average consumption of the poor. Especially the beneficiaries of public works programs that provide workdays at special periods of the year cannot be considered as having decent jobs and being covered by social protection. Therefore these types of programs are not a means of transitioning from the informal to the formal economy.

In rural areas, extremely vulnerable populations need special support at certain periods of the year and/or in certain years. Labour intensive public works are a widespread type of safety net that provides a certain number of workdays to seasonally unemployed populations or populations hit by external or climatic shocks.

Chart 1: Typology of social safety nets

Source: World Bank (2015).

One of the most renowned and of the largest of such schemes, is the MGNREGA (Mahatma Gandhi National Rural Employment Guarantee Act) launched in 2005 in India. It is a labour law and social security measure aiming to enhance livelihoods in rural areas by providing at least 100 workdays per year to volunteering adults within 5 km of residence and paid at minimum wage: if work is not provided within 15 days of application, applicants are entitled to an unemployment allowance. It secures all citizens the right to work, which they are entitled by the Constitution. One-third of employment is reserved for women and equal wages are provided to women and men. It was calculated that since its inception, the programme resulted in the payment of more than 12 billion person-days of employment. The programme also aims to create durable assets such as roads, dams, wells, canals, etc. Another important outcome of the scheme is that wage corruption declined thanks to the payment of wages through bank and post office accounts and community monitoring.

Not all safety nets are uni-dimensional and examples of multi-pronged programs seem to be more effective towards ensuring beneficiaries with lasting effects. Such types of safety nets deserve attention: For instance the BRAC Targeting the Ultra-Poor (TUP) Program and the HARITA (Horn of Africa Risk Transfer for Adaptation) initiative.

|

Box 21 – Building Resources Across Communities Programme The BRAC’s graduation approach targeting the ultra-poor is one of such examples and presents the advantage of a strong and reliable empirical evaluation. BRAC stands for Building Resources Across Communities (initially Bangladesh Rehabilitation Assistance Committee). It is the largest Non Governmental Organisation for international development in the world and is supposed to reach more than 126 million people in 14 countries. In 2002, BRAC developed the Targeting the Ultra-Poor (TUP) Programme through a graduation approach after noticing that the social safety nets failed to reach the extremely poor. The approach addresses the social, economic and health needs of poor families simultaneously by combining the satisfaction of immediate needs with longer-term interventions in life and technical skills training, asset transfers, enterprise development and savings towards more sustainable livelihoods (see Chart 2 below). Selected through a participative process the beneficiaries are given a productive asset chosen from a list, and the corresponding training, as well as life skills training and consumption support during a given period. They have access to savings schemes and health services. All these supports are supposed to provide the households with a ‘big push’ for a self-employment activity. The program is costly, reaching an amount per household equivalent to the household consumption as measured by the baseline survey. In fact BRAC implements two approaches, one for the Specially Targeted Ultra-Poor (STUP) who receive the productive asset, and the second for the Other Targeted Ultra-Poor (OTUP), marginally less deprived, who receive a soft loan for acquiring the asset. In Bangladesh, the program reached more than 600,000 households and its replication was decided in 20 countries. In 2006, the approach was adapted and tested in 8 countries. A randomized evaluation through control trials was conducted on 6 of these countries (India, Pakistan, Ethiopia, Ghana, Honduras, Peru), the results of which were published in Science (Banerjee, Duflo et al., 2015) looking at the progress at the end of the program and one year later. Measuring the impact of the program on 10 key outcomes (consumption, food security, productive and household assets, financial inclusion, time use, income and revenues, physical health, mental health, political involvement and women’s empowerment), the study found significant impact on all of them, one year after the end of the project or 3 years after the transfer of the productive assets. And in 5 out of 6 countries, the extra earnings exceeded the program cost. The study concludes that the multifaceted approach is sustainable and cost-effective. |

Chart 2: The graduation approach of the TUP Program

Source: BRAC, 2016.

|

Box 22 – HARITA Initiative The HARITA (Horn of Africa Risk Transfer for Adaptation) initiative, pioneered in Ethiopia by Oxfam America, the Relief Society of Tigray (REST) and Swiss Re, is another multi-pronged program. It is at the origin of the R4 Rural Resilience Initiative (with the World Food Programme). R4 currently reaches almost 200,000 people in Ethiopia, Senegal, Malawi and Zambia (32,000 with insurance) through a combination of four risk management strategies: improved resource management through asset creation (risk reduction), insurance (risk transfer), livelihoods diversification and microcredit (prudent risk taking) and savings (risk reserves). The Harita Programme in Ethiopia made large use of the “weather index insurance” (WII). The WII is a relatively new but innovative approach to insurance provision that pays out benefits on the basis of a predetermined index (e.g. rainfall level) for loss of assets and investments, primarily working capital, resulting from weather and catastrophic events, without requiring the traditional services of insurance concludes assessors. It also allows for quicker and more objective insurance settlement processes to be (Madajewicz and al., 2013). The project made payments contingent on recorded rainfall rather than yields. Basing payments on rainfall eliminated the costly moral hazard problems involved in verifying yields on smallholder farms and therefore made the premiums more affordable. In the event of a seasonal drought, insurance pay-outs were triggered automatically when rainfall dropped below a pre-determined threshold at a pre-determined time during the growing season. HARITA relied on satellite data for rainfall measures. How to pay for this insurance? In the HARITA team’s conversations with farmers, the farmers themselves suggested a solution – they could pay for insurance with their labour. Oxfam America worked with the Relief Society of Tigray and the Government of Ethiopia to build an “insurance-for-work” program on top of the government’s “food- and cash-for-work” Productive Safety Net Program (PSNP), a well-established program that serves eight million chronically food-insecure households in Ethiopia. The resulting innovation allowed cash-poor farmers who were PSNP participants the option to work for their insurance premiums on the risk reduction activities. During the 2010 growing season, 80% of farmers who bought insurance were PSNP participants who paid with labour, while in 2012 93% paid with labour in those villages in which farmers had the option to pay with labour. Risk reduction activities began after farmers had purchased insurance since the amount of insurance purchased determined the amount of labour that farmers had to provide. The evaluation points out that the insurance pay-out may improve livelihoods by allowing farmers to preserve food consumption and/or their asset holdings after a drought and to repay their loans. Farmers who receive an insurance pay-out may not need to sell assets in order to feed their families and to repay loans. Therefore, farmers may maintain higher yields in subsequent seasons, preserving food security and livelihoods. These effects may also influence migration patterns since men from farming household may be less likely to migrate if livelihoods at home improve. The second effect is on productive investments and consumption in growing seasons with good rainfall. The threat of drought may cause farmers to invest less in all seasons and to avoid borrowing to finance investments because farmers worry that investments will be wiped out by drought. The promise of an insurance pay-out that will help to repay loans and buy food in case of a drought may enable farmers to increase investments, translating into higher yields, assets, and incomes in good seasons, and therefore improved food security and livelihoods in all seasons. |

Beyond their direct impact on beneficiaries the cash transfers and other forms of social safety nets also impact non-beneficiary households and the local economy at large. As a matter of fact, the cash inflows can play the role of income multipliers and they have been measured with an innovative village economy model, called the LEWIE (Local Economy-Wide Impact Evaluation) model and coined for the cash transfer programmes in Kenya, Lesotho, Ghana, Malawi, Zambia, Zimbabwe and Ethiopia. It was shown that the income multipliers ranged from 2.52 in Ethiopia to 1.34 in Kenya, account being taken of increased prices (Universal Social Protection, 2016).

1.2 Variety of risks covered

ILO Convention 102 (1952) indicates the 9 main branches of social protection: healthcare, sick leave and allowances, unemployment benefits, old age pensions, accident at work and professional illness benefits, family allowances, maternity leave and benefits, invalidity and survival allowances.

Among the various risks constituting a complete social protection system, health coverage seems the most basic and the one to be given the highest priority provided that sickness and exposition to various diseases remain the major causes for the absence or insufficiency of income from work. Many countries have enshrined universal health coverage - a target of SDG’s Goal 3 - in their policy agenda. While this type of coverage can be based on social contributions paid by employers and employees and even self-employed within the usual social security systems, it is also the type of risk that can be easily covered by the private sector. As a matter of fact savings can be collected through micro-finance schemes, not only in order to provide micro-credit, but also as insurance for health coverage, or rather as a right of entry into a mutual insurance (see infra the example of GESCO in the AVSI project in Côte d’Ivoire).

Two other risks affecting the capacity of the poor to earning a living are occupational safety and health and regarding women, maternity.

Because they generally operate their activities without any protection, informal workers are, more than others, subject to occupational injuries or occupational diseases: occupational safety and health are therefore a major concern for populations working in the informal economy. However it is much more difficult to sensitise people to such risks and to persuade them saving money to this aim. This is why projects generally address this issue through the improvement of protection at workplace, for instance by distributing clothes or equipment (gloves, boots, masks, helmets, masks, etc.). Insurance against such risks can be covered in a similar ways as health, for those workers who are especially subject to these risks.

Maternity leave and all issues about childcareare also important for women in the informal economy, because they correspond to periods during which their income-generating activities may be restricted and therefore be insufficient: Mothers must come back as soon as possible to their informal occupations, often to the detriment of their child’s health. It is a domain where the public sector is generally unable to play its role as far as the informal economy is concerned, but it should be a concern for projects.

Among the other risks to be covered are the old-age pensions, but this type of risk is rather a responsibility of the state in that it is much more difficult to make it taken into consideration by poor populations for whom short-term needs are of greater concern that long-term issues. Furthermore it is a domain where community solidarities continue to play their role: Large families and a great number of children are the usual means to cope with old age in traditional societies. When comes the time for the elderly of the inability to work, it is up to the family to take care. However, economic crises, ageing and the rise of unemployment have put extended families to pressure and made it more and more difficult for the progeny to take care of ascendants. ‘Individualisation’ is a consequence of globalisation and urbanisation and has progressively eroded ‘community solidarities’ behaviours (Marie, 2008).

As regards the protection against unemployment risk, rare are the developing countries that included such benefits in their social security systems (in Algeria for instance, the unemployment benefits were implemented at the time structural adjustment and to accompany the downsizing of the public sector, then it turned into a fund devoted to the provision of credit for the creation of micro-enterprises). A guarantee of basic income for the unemployed would be difficult to implement in countries with high unemployment and underemployment rates and scarce resources. Still for a long time labour intensive public works safety nets will be the only means to provide the poor with a minimum number of workdays and a minimum income per month. In some countries poor farmers have been authorised to mop up their debt with such workdays. However safety nets as such are not a means for ensuring the transition from the informal to the formal economy because they are not creating decent jobs.

But there is a long way to reach such objectives. In many countries, only paid employees of the formal sector have access to these minimum rights. Even in the formal sector, health services are frequently not yet accessible at reduced costs. For the majority of people, relying on social assistance programmes remains the only way to benefit from health care services and obtain a minimum income. These programmes still do not target the majority of the population who work in the informal economy. Reliance on self-help community-based groups is their primary resort, i.e. they use their own savings.

Despite international recommendations, ensuring the minimum standards of social protection for people depending on the informal economy remains a challenging objective for projects. Micro-finance institutions are often the only tool that can be reliably used towards achieving this aim.

As shown in section 1 above, as early as the 1970s, the ILO has been the first international institution to show interest in the informal economy (and especially the informal sector) and to take measures or adopt recommendations for the design of policies addressing this sector, as a source of jobs in a period when unemployment was on the rise. Transforming the negative concept of informality (and the negative criteria that define it) into the more positive view of “decent work” (with positive criteria, among which the benefits of the various dimensions of social protection take place: ILO, 1999), the ILO came to define a social protection floor (ILO 2011) and adopted the recommendation 202 (ILO, 2012: see box hereafter) and more recently the recommendation 204 – quasi-unanimously adopted by the International Labour Conference in 2015 - on the transition from the informal to the formal economy (ILO, 2014 and 2015).

|

Box 23 - The social protection floors In 2012, the International Labour Conference adopted recommendation 202 on social protection floors: “Social protection floors are nationally defined sets of basic social security guarantees that should ensure, as a minimum that, over the life cycle, all in need have access to essential health care and to basic income security which together secure effective access to goods and services defined as necessary at the national level.” Recommendation 202 applies to all, including workers in the informal economy. “National social protection floors should comprise at least the following four social security guarantees, as defined at the national level: 1. access to essential health care, including maternity care; 2. basic income security for children, providing access to nutrition, education, care and any other necessary goods and services; 3. basic income security for persons in active age who are unable to earn sufficient income, in particular in cases of sickness, unemployment, maternity and disability; 4. basic income security for older persons.” |

These recommendations have convinced and encouraged governments to make efforts towards the extension of their social security systems. Countries such as South Africa or Kenya have even enshrined the right to social protection in their constitutions.

It is thanks to the ILO that the extension of social protection is henceforth tightly linked to the process of formalisation, not only because the absence of payment of social contributions is a criterion for defining informal employment (or non decent work), but also because the traditional systems of social security revealed to be unsustainable in the long run with the ageing of populations, the rise in the number of pensioners and the tightening of the base for the payment of social contributions (mainly the wage bill of the formal/public sector).

The World Social Protection Report 2014-15 (ILO, 2015) recalls that according to ILO estimates, in 2012 “only 27% of the working-age population and their families across the globe had access to comprehensive social security systems. In other words, almost three-quarters, or 73 per cent, of the world’s population, about 5.2 billion people, do not enjoy access to comprehensive social protection”: A global figure that is close to our estimates for employment in the informal economy.

This is why the reflexion on social protection is at the core of the policies addressing the informal economy, especially the policies for the transition to the formal economy.

Several examples of such policies can be presented.

1.3 Examples of national policies

Tunisia is said to have one of the most extended social security system in Africa, both horizontally (by the number of professions or populations groups covered: from civil servants to small farmers and domestic workers) and vertically (by the number of risks covered: from health to old age pensions). Informal employment (including agriculture) that is a measure of the labour force not covered by social security did not exceed ¼ of total employment by 2011, year of the revolution, until its recent increase (up to per 32 cent in 2015).

In parallel with the contributory system of social protection (based on the payment of a contribution by the workers (either own-account or paid, and the employers), a large distributive system was implemented since the end of the 1980s through the national programme for support to needy families (PNAFN) that benefits today to more than 230.000 households: 8,5 per cent of the 2,713,000 households enumerated in 2014 and an increase of some 100,000 households since 2010. The PNAFN is a programme of cash transfers (a monthly money order of 120 Dinars equivalent to 45% of the legal minimum salary) conditioned to the absence or insufficiency of income, accompanied by a free health care card for all members of the household. In addition to the programme, cards for health care at reduced cost were also attributed to more than 600,000 individuals.

In a period when the country has enshrined social inclusion into its new Development Plan 2016-2020 and its Vision for Tunisia 2020 and made of the safeguard of its social protection system a high priority, as well as the perspective of the universal health coverage, an assessment of the weaknesses and disequilibria of the social protection system in its various dimensions was necessary. All the more so as further to the adoption of the recommendation 204 by the 2015 International Labour Conference - the transition from the informal to the formal economy has become another priority for the government, that requires a more in-depth knowledge of the roots and dynamics of the informal economy.

According to a report prepared on Social Protection and the Informal Economy for the Centre of Research and Social Studies (CRES) and the African Development Bank, (Charmes and Ben Cheikh, 2016), one of the dilemma of the Tunisian social protection system is that the most generous schemes of the contributory system (for instance the special scheme for the low income workers) and of the distributive system have progressively nibbled and contaminated the equilibrium of the whole system. Critics have been addressed to the distributive system regarding its weak targeting (not even to say its “clientelism”). In a report prepared for the ILO on “the Tunisian youth and the informal economy”, it was shown that a high proportion of the new entrants to the labour market worked informally (more than 75 per cent) and a non-negligible proportion of them accepted to do so in order to continue benefitting of the free or reduced cost card for health, that they would have lost if they had been formally declared and had contributed to the normal schemes of social security (Charmes, 2015).

Although there is a kind of consensus among social partners (trade unions and employers’ organisations) about such a state of affairs, the increasing deficit of the social security funds leads the government, within a general will to push toward the transition from the informal to the formal economy, to check whether or not a significant proportion of the households benefitting from the distributive system could be brought back to one of the contributory schemes. At the request of the Ministry of Social Affairs, CRES conducted a survey for the evaluation of the distributive programmes that confirmed that the population of beneficiaries tended to become younger and that some 27% of the beneficiaries were earning income high enough to allow them to contribute to the schemes (CRES, 2015).

Yet another potential source of contribution is the under-declaration of the level of wages in the formal sector and a balanced policy must also target the shadow economy in the formal sector.

In many respects the social security system in Algeria (where informal employment has been decreasing during the recent period and did not exceed 38.5% of the total labour force in 2015) is also among the most progressive and experiences the same difficulties. The Finance Law for the year 2015 precisely refers to the Recommendation 204 on the transition from the informal to the formal economy aiming at “making of the country one of the precursors in the broadening of social protection to the informal sector and the implementation of an incentivising process towards formalising this sector and reducing it, in conformity with the new international ILO conventions for the next decade”.

The objective is to cover the active occupied persons not subject to the social security system in force, by voluntary affiliation on the basis of a contribution equal to 12% of the legal minimum salary during a transition period: the potential beneficiaries of this measure are estimated to 1 million (and 3 million with the entitled family members) and by aggravating controls and sanctions against employers who do not declare or who under-declare their employees.

Further to the adoption of the Law, the National Social Security Fund has tried to incentivise the informal workers, especially the own-accounts workers, to join a special transitional scheme at the Fund for wage earners (CNSS), as a first step toward their registration to the Fund for own-account workers (CASNOS) (Charmes and Remaoun, 2016).

These are two examples of national policies that have been designed and implemented in the wake of the ILC recommendation 204. They show how governments and national institutions conceive the transition from the informal to the formal economy.

Côte d’Ivoire where the social security in the formal sector only covers old age pensionshas recently launched universal health coverage, starting however modestly with the public sector. In such a case, progress will be achieved through the private sector and the intervention of projects at field level as shown in the following section.

1.4 Role and impact of projects or Civil Society Organizations for the extension of social protection

Capacity strengthening is on the agenda of most development policies and projects. It applies to public institutions, private and community institutions as well as individuals. Capacity strengthening of public institutions can help meet the goals of formalising the informal economy by expanding its benefits to the most remote and vulnerable populations.

Projects aiming at enhancing the livelihoods of vulnerable populations dependent on the informal economy have nonetheless found original ways and means of achieving the objective of expansion of coverage. This includes examples of national health insurance systems that combine organising small informal operators with providing outreach. It also includes incentivising local and central administrations in charge of the national health insurance system.

The basic principle is that public service providers should go to the population to offer the said services and collect corresponding taxes or premiums instead of waiting for populations to come forward on their own.

In countries where social contributions for health coverage are not recovered through the employers on the salaries they pay to their employees, and/or where own-account workers represent an important share of the workforce, the individuals have to pay their contributions directly to a national health fund and in this case it is expected from the people that they behave with the consciousness of the necessity to be insured in case of illness or injuries. The National Health Insurance Funds in Ghana is of this type, while in Côte d’Ivoire, such a National Fund does not exist. It is interesting to see how a system of universal health coverage can be achieved in these two countries.

In Ghana the National Health Insurance System (NHIS) was established under the Act 650 in 2003 in order to“provide basic health services to persons resident in the country through mutual and private health insurance schemes”. Members receive a card, which enables them to go to hospital and benefit from general outpatient services, inpatient services, oral health, eye care, emergencies and maternity care, including prenatal care, normal delivery, and some complicated deliveries, without direct payments. In 2008, nearly 54% of the population were covered, but vulnerable groups failed to benefit from the scheme. Therefore the government decided that all children under 18 and all pregnant women should receive a card (Abebrese, 2012).

The NHIS was also successfully involved in facilitating the registration and membership card renewal of an EC supported project’s beneficiaries (Volume 4.1: Charmes and Zegers, RNSF, ARS Progetti, 2016). The project focused, among other aspects, on market access of women shea producers through cooperative action. Using a combination of sensitization, logistics support, and techniques for facilitating registration and organizing women producers it was possible to reach the goal of improved access to these public services.

Meetings with the staff of regional offices of NHIS were used to convince them to participate in sensitizing clients on the importance of the NHIS and help them understand that the project valued their role as service providers.

Logistics support, such as vehicle and a public address system, was also provided to facilitate their travel to the sites for mass registration.

NHIS staff gave presentations of the role of their institution and the benefits for the population in the project field sites. The NHIS staff was asked numerous questions since many women were unaware of the existence of such health insurance schemes. They also had to listen to complaints about non/late delivery of cards, difficulties in renewing cards as well as about the frustrations that card bearers encountered at various delivery points. This exposure helped make the NHIS staff more aware of the harsh conditions of remote and vulnerable populations.

Techniques for facilitating registration included getting women to make contributions in instalments towards registration and renewals. It also included scheduling bulk registrations in the communities thus extending registration operations beyond the projects’ beneficiaries through a cascading effect. Project officers also contributed by picking up the expired cards of women and bringing them to the NHIS offices.

Women producers have been organised in community social funds (CSF) that were connected to Micro Finance Institutions to obtain financial support for their production activities but also for NHIS registration. This allowed the CSF members to share their health risks as they can pool resources together through the CSF to access healthcare. An increased attendance to health facilities has been observed with earlier treatment of sicknesses/diseases.

NHIS officials now travel to renew expired cards and register new clients as a result of the collaboration between the NHIS and the shea associations.

The good practice described is an illustration of the role that civil society organisations can play in complementing government institutions to fulfil development agendas such as the achievement of universal health care services.

The logistical support provided may raise the question of the sustainability of the good practice. It is up to the NHIS administration to incentivize its staff through the achievement of quantitative goals for new registrations and renewals.

Such systems of universal health coverage exist in other regions of the world: Ghana NHIS is very similar to the Thailand’s UC Scheme (earlier known as the “30 Baht Scheme”, a very modest sum) that guarantees any Thai citizen access to health services provided by designated district-based networks of providers (consisting of health centres, district hospitals and cooperating provincial hospitals). Individuals are able to access a comprehensive range of health services, in principle without co-payments or user fees, including both inpatient and outpatient services and maternity care, furnished by public and private providers, within a framework which emphasizes preventive and rehabilitative aspects (Lim, 2016).

Conducting outreach and incentivising local or central administrations (Social security, health insurance services) to search and convince informal economy operators to register rather than wait for them to come and register on their own is a good practice that has been recently implemented in various contexts.

In Tunisia for example, under the programme Tunisia Inclusive Labor Initiative TILI (Global Fairness-ISTIS-TAMSS, 2013), the Ministry of Labour and especially the Labour Inspection with the support of TAMSS association has conducted pilot-actions towards crafts and small businesses in 7 governorates in order to sensitise them to fiscal obligations, social protection and labour laws as it is often taken for granted that informal operators do not know longer what is to be done for coming back to legality: the absence of information, the fear of bureaucracy and corruption raise barriers against the transition to the formal economy. Workshops were organised for informal operators in the presence of all administrations (Tax, social security, customs, governorates) to listen to their voice and build a climate of mutual trust and dialogue. But the generalisation of such pilot actions would require the strengthening of human and financial resources.

In countries where bureaucracy is synonymous of clientelism and patronage, such actions are also a means for providing informal operators with some kinds of relationships within the bureaucracy and supporting them in building social capital.

As indicated above, Côte d’Ivoiredecided to pursue an objective of universal health coverage, starting with the public sector. Considering that with such an agenda it would take years before handicrafts take their turn, the AVSIintegrated project in support to the empowerment of craftsmen and women of Côte d’Ivoire (one among the 17 on-going projects that are part of the present programme “Research, Network and Support Facility” (RNSF)) included health coverage for its beneficiaries among its long-term objectives. The AVSI project, conducted in partnership with the National Chamber of Crafts in Côte d’Ivoire, aims at improving the skills of its beneficiaries, their social inclusion and the institutional framework within which they operate. The implementation of a health coverage mutual fund is conceived for ensuring the sustainability of the other dimensions of the project (Volume 4.4,). This good practice has already been described in the section on “organising” supra.

The project has put in place Savings and Community Solidarity Groups (GESCO) and, through these groups, collected initial amounts then weekly amounts arousing emulation between villages. Despite the success of the approach, it would have been difficult however to reach the minimum amount necessary to create a mutual Fund for the handicrafts. Too long delays would have disappointed the strong expectations and would have weakened the trust of the population in a context where previous failures have left traces. Therefore, AVSI suggested to contribute to various existing and successful and efficient regional mutual funds of agricultural planters or other trades, and modulate the services according to the financial capacities of craftsmen: it is a flexible model that can be adapted according to the regional opportunities and is a preliminary step towards an independent mutual insurance for crafts.

In this approach, AVSI is supported by the Support Programme for the mutual health insurance strategies (PASS) at the regional level of the WAEMU countries.

In India, the Self Employed Women’s Association’s (SEWA) integrated insurance scheme, or VIMO SEWA, has three components – life insurance, asset insurance and health insurance. It has over 102,000 members and was a response by SEWA to the concerns of members that the majority of what they earn is spent on health costs, and ill health was a major cause of loan default in their savings scheme. The health insurance helps cover the cost of seeking necessary medical attention. In so doing, it helps to avoid further loss of income in addition to that already caused by the illness or injury, such as loss of earnings. The reduction in cost of treatment is an important incentive for workers to seek medical attention when needed rather than risk continuing to work and further compounding health problems (Lund, 2009).

Recapitulating some good practices in the field of social protection extracted from more than two hundreds projects, Zegers mentions (RNSF, ARS Progetti, 2016, Volume 4.2):

a) the inclusion of a range of stakeholders (among which government, employers’ and workers’ organisations, and civil society groups and other non-state actors) related to the informal economy in capacity-strengthening and decision-making on social protection issues as it helps raise their awareness and strengthens their ownership of the related processes;

b) the promotion of registration of the informal workers in social security systems by working directly with the informal operators and their workers;

c) the emphasis on the dissemination of information on social protection resources that may be available. Where associations of workers dependent on the informal economy cannot provide access to social protection themselves, support should be provided establishing linkages of operators and workers in the informal economy with social protection services through exchanges and meetings. A reason for this is that changes in revenue collection and management systems become more effective and acceptable to the people when they better understand what they are likely to gain from the changes;

d) the provision of project beneficiaries with the best available insurance solutions in line with their needs and their disposable assets: it is necessary to obtain workers’ opinion and insights to understand which option could be considered as the most suitable;

e) the necessity of sound advocacy and training on the linkages between social protection and employment toward a better integrated approach in the design of projects;

f) finally, it was noted that targeted social protection (including safety nets) and investments in infrastructure and production technology may offer extremely vulnerable people better alternatives than support for micro-credit.

For WIEGO, social protection is a high priority for informal workers who list, after the increase and sustainability of their income, access to health services, child care and savings/security for the old age, among their highest priorities. Based on its wide experience, WIEGO considers that informal workers should be integrated, wherever possible, into formal schemes, rather than being covered through small schemes especially designed for them. Short-term safety nets are definitely not enough and social protection for informal workers must be mainstreamed and be a long-term commitment (http://wiego.org/wiego/social-protection-informal-workers). Although not fitting with such requirements, it is however necessary to mention safety nets as they are still, in many countries, the only policies meant to provide the poor with a source of income.

1.5 Back to taxation

According to the World Bank and the ILO allied within the Universal Social Protection Initiative, today more than 30 low and middle-income countries have universal or nearly universal social protection programs, and over 100 others are “scaling-up social protection and fast-tracking expansion of benefits to new population groups. Universal social protection is most commonly achieved for old-age pensions. Universal social protection for children is also a reality in some countries”. They however recognise that it requires appropriate and important sources of financing and that there are several options to this aim:

- Re-allocating public expenditures;

- Increasing tax revenues, including revenue generated from taxation of natural resources;

- Using the reductions of debt or debt servicing;

- Expanding social security coverage and contributory revenues.

It is particularly stressed that “enforcement of social security revenue collection may result in higher tax collections, particularly in countries with young demographic pyramids. Higher tax revenues can in turn support the promotion of statutory programs.”

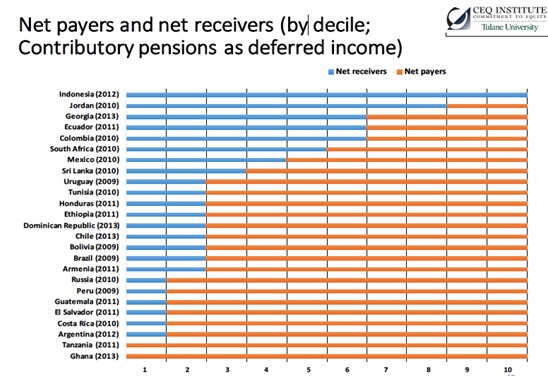

These remarks bring us back to the issue of taxation of informal activities (§section II, Chapter 1). Until recently and still often, social protection policies and fiscal policies were treated separately and it is now widely admitted that they should be treated jointly. Observing that in some countries such as Ethiopia, almost 70% of the poor pay tax, and that subsidies mainly benefit the rich, researchers have developed a new concept of “net social protection” (Lustig, 2016b). According to them, analysing the impact of spending on social protection without the impact of financing on the poor is useless: When financing is added in the picture, the net effect of social spending on social protection can increase poverty.

Chart 3 summarises the findings: in Tunisia and Ethiopia the first two deciles are net receivers whereas the others are net payers; in Ghana and Tanzania, all deciles are net payers.

Chart 3: Net payers and net receivers to the fiscal system by decile

Source: Lustig (2016a and b). http://commitmentoequity.org/

The discussion on transition from the informal to the formal economy is therefore inseparable from the discussion on social contract, social inclusion, citizenship and the payment of taxes. For some policy makers and observers presumptive taxes are the means to bring as many people as possible into the tax system, while for others citizenship is not linked to the payment of taxes.

1.6 Conclusions

In conclusion, it seems clear that for most of the international and bilateral institutions, as well as governments, social safety nets are the solution that will allow achieving the goal of universal social protection. If so, the path is still long towards the transition from the informal to the formal economy. Of course providing workdays to poor populations is positive but it cannot be considered as the unique solution towards achieving such an ambitious goal.

Nicholas Taylor, a former head of sector Employment, Social Inclusion and Social Protection at EU-DEVCO, states that “countries are now moving away from a panoply of small fragmented programmes mostly managed and funded by donors or implemented by NGOs in very small contexts (…) into a very different framework where countries want to have this as part of national social policy.” (http://capacity4dev.ec.europa.eu/article/how-expand-social-protection-sustainably)

However, as WIEGO puts it, informal workers should be integrated, wherever possible, into formal schemes, rather than being covered through short-term safety nets that are not enough. And as a participant to a recent OECD-EU meeting of experts on social protection stressed in the concluding remarks, time may have come to move

- From targeting to universal coverage,

- From conditional to non-conditional transfers,

- From fragmented to more comprehensive approaches,

meaning that it is time for social protection to be given the highest priority and to be given its entire contents.

Social protection for informal workers must be mainstreamed and be a long-term commitment, but good practices and lessons learned from projects have still a role to play in the implementation of such national policies. In this respect national policies could play a role of coordination. Furthermore inefficient bureaucracies, immersed in clientelist practices and cronyism and devoid of resources, need to be sensitised, incentivised and accompanied by grassroots organisations in order to operate their mutation, not to say their revolution: serving the people rather than having the people at their service.

1.7 References

- Abebrese Joyce (2012), Social protection in Ghana, An overview of existing programmes and their prospects and challenges, Friedrich Ebert Foundation, 21p.

- African Union (2011), Social Protection Plan for the Informal Economy and Rural Workers 2011-2015 (SPIREWORK), Addis Ababa, 18p.

- Banerjee Abhijit, Duflo Esther, Goldberg Nathanael, Karlan Dean, Osei Robert, Parienté William, Shapiro Jeremy, Thuysbaert Bram, Udry Christopher (2015), ‘A multifaceted program causeslasting progress for the very poor:Evidence from six countries’ in Science 15 May 2015, Vol 348 Issue 6236.

- Benjamin Nancy with Kathleen Beegle, Francesca Recanatini and Massimiliano Santini(2014), Informal Economy and the World Bank, Policy Research Working Paper N°6888, May, 2014.

- BRAC (2016), BRAC’s Ultra-Poor Graduation Programme: An end to extreme poverty in our lifetime,

- Charmes Jacques (2003), ‘Le capital social: quelques conceptions et données empiriques tirées du contexte africain’, in Jerome Ballet et Robert Guillon (eds.), Regards croisés sur le capital social, L’Harmattan, 184p.

- Charmes Jacques (2012), The Informal Economy Worldwide : Trends and Characteristics, In: Margin: The Journal of Applied Economic Research, 2012 6 :103, May 2012

- Charmes Jacques (2015), La jeunesse tunisienne et l’économie informelle, BIT, Tunis, Genève, 99p.

- http://www.ilo.org/employment/Whatwedo/Instructionmaterials/WCMS_444912/lang--fr/index.htm

- Charmes Jacques et Nidhal Ben Cheikh (2016), ‘Protection sociale et économie informelle en Tunisie, Défis de la transition vers l’économie formelle’, CRES et Banque Africaine de Développement, Tunis, 92p. http://www.cres.tn/index.php?id=118

- Charmes Jacques et Malika Remaoun (2016), L’économie informelle en Algérie. Estimations, tendances, politiques, BIT, Alger, 105p.

- Charmes Jacques and Mei Zegers (2016), Identification of Innovative Approaches to Livelihood Enhancement, Equity and Inclusion of People Dependent on the Informal Economy, Vol.4.1 Good Practices and Lessons Learned. Extracted from 33 Projects Selected Under the 2009 EC call for Proposals: “Investing in People. Promoting social cohesion, employment and decent work. Support for social inclusion and social protection of workers in the informal economy and of vulnerable groups at community level”. RNSF, ARS Progetti.

- CRES (2015), Enquête d’évaluation de la performance des programmes d’assistance sociale en Tunisie. Pour optimiser le ciblage des populations pauvres et freiner l’avancée de l’informalité, CRES,Tunis. http://www.cres.tn/uploads/tx_wdbiblio/resume_executif_3_avril_2015.pdf

- Del Ninno Carlo and Mills Bradford, Eds. (2015), Safety Nets in Africa: Effective Mechanisms to Reach the Poor and Most Vulnerable, Washington, 267p.

- Global Fairness-ISTIS-TAMSS (2013), Survey of Informal Workers in Tunisia, Study Report, Tunis, 65p.

- ILO (1999), Decent Work, Report of the Director General, International Labour Conference, 87th Session, Geneva,

- ILO (2011), Social Protection Floors for Social Justice and a Fair Globalisation, Report IV (1), ILC 2012. http://www.ilo.org/wcmsp5/groups/public/---ed_norm/---relconf/documents/meetingdocument/wcms_160210.pdf

- ILO (2012), Social Protection Floors Recommendation R202, ILC 2012. http://www.ilo.org/dyn/normlex/en/f?p=NORMLEXPUB:12100:0::NO::P12100_INSTRUMENT_ID:3065524

- ILO (2014), Transitioning from the informal to the formal economy – Report V. International Labour Office (ILO), Geneva. International Labour Conference, 103rd Session, 2014.

- ILO (2014), Transitioning from the informal to the formal economy – Report V(2). International Labour Office (ILO), Geneva. International Labour Conference, 103rd Session, 2014.

- ILO (2015), Transitioning from the informal to the formal economy – Report V. International Labour Office (ILO), Geneva. International Labour Conference, 104th Session, 2015.

- ILO (2015), Recommendation 204 - Recommendation concerning the Transition from the Informal to the Formal Economy, adopted by the Conference at its one hundred and fourth session, Geneva, 12 june 2015

- ILO (2015), World Social Protection Report, Building economic recovery, inclusive development and social justice 2014/15, Geneva, 336p. http://www.ilo.org/wcmsp5/groups/public/---dgreports/---dcomm/documents/publication/wcms_245201.pdf

- Kapaz, Emerson; Kenyon, Thomas. 2005. The Informality Trap: Tax Evasion, Finance, and Productivity in Brazil. Viewpoint. World Bank, Washington, DC. © World Bank.

- https://openknowledge.worldbank.org/handle/10986/11201 License: CC BY 3.0 Unported.”

- Lim Lin Lean (2015), Extending Livelihood Opportunities and Social Protection to Empower Poor Urban Informal Workers in Asia, OXFAM-WIEGO-Rockefeller Foundation, Bangkok, 89p.

- Lund Francie (2009), Social Protection and the Informal Economy: Linkages and Good Practices for Poverty Reduction and Empowerment, WIEGO,

- Lustig Nora (2016a), Fiscal Policy, Inequality, and the Poor in the Developing World, Tulane University, Economics Working Paper 1612, October.

- Lustig Nora (2016b), Fiscal Redistribution in Low and Middle Income Countries, Tulane University CGD and IAD, presented at DevTalks, Development Centre OECD, Paris, October 10, 2016.

- MadajewiczMalgosia, Haile TsegayAsmelash, Norton Michael (2013), Managing Risks to Agricultural Livelihoods: Impact Evaluation of the Harita Program in Tigray, Ethiopia, 2009–2012, Impact evaluation, OXFAM America, Boston.

- Marie Alain, 2008, ‘Du sujet communautaire au sujet individuel, Une lecture anthropologique de la réalité africaine contemporaine’, in Marie Alain (ed.), 2008, L’Afrique des individus, Itinéraires citadins dans l’Afrique contemporaine (Abidjan, Bamako, Dakar, Niamey), Karthala, Paris, 442p. (‘From community subject to individual subject, An anthropological reading of contemporary African reality’ in The Africa of individuals, Urban itineraries in contemporary Africa).

- Oduro Abena D. (2010), Formal and Informal Social Protection in Sub-Saharan Africa, Paper prepared for the Workshop “Promoting Resilience through Social Protection in Sub-Saharan Africa” organised by the European Report on Development in Dakar,

- 28-30 June 2010.

- Palmade, Vincent; Anayiotos, Andrea. 2005. Rising Informality. Viewpoint: Public Policy for the Private Sector; Note No. 298. World Bank, Washington, DC. © World Bank.

- https://openknowledge.worldbank.org/handle/10986/11209 License: CC BY 3.0 Unported.”

- Schneider Friedrich, Andreas Buehn and Claudio E. Montenegro (2010), Shadow Economies all over the World: New Estimates for 162 Countries from 1999 to 2007, Policy Research Working Paper No. 5356, The World Bank Development Research Group, Poverty and Inequality Team, Europe and Central Asia Region Human Development Economics Unit, July 2010

- Universal Social Protection (2016), Economic and productive impacts of national cash transfers programmes in Sub-Saharan Africa. http://www.social-protection.org/gimi/gess/RessourcePDF.action?ressource.ressourceId=53945

- Vuarin Robert, 1993, ‘Quelles solidarités sociales peut-on mobiliser pour faire face au coût de la maladie ?’ in Brunet-Jailly Joseph (ed.), 1993, Se soigner au Mali, Paris, Karthala. (‘Which social solidarities can be mobilised for coping with the cost of sickness’ in Brunet-Jailly (ed.), ‘To be cured in Mali’).

- Vuarin Robert, 2000, Un système africain de protection sociale au temps de la mondialisation, Paris, L’Harmattan, 252p. (An African system of social protection at the time of globalisation).

- World Bank (2012), Managing Risk, Promoting Growth: Developing Systems for Social Protection in Africa, The World Bank’s Africa Social Protection Strategy 2012-2022, Washington, 77p.

- World Bank (2015), The State of Social Safety Nets 2015, Washington, 164p.

- World Bank and ILO (2015), A shared mission for universal social protection, Concept note, 5p.

- Zegers Mei (2016), Identification of Innovative Approaches to Livelihood Enhancement, Equity and Inclusion of People Dependent on the Informal Economy, Volume 4.2: Recommendations Based on Analysis of a Range of Development Agencies on Support to People Dependent on the Informal Economy, RNSF, ARS Progetti, 213p.

[1]These conceptions of social security and social protection slightly diverge from ILO’s. For the ILO, social security is the generic term encompassing social protection and social assistance.